There are few rituals more American than a stop at a gas-station convenience store. It starts with the badly needed fill-up or bathroom break, then progresses to an impulse food-and-beverage buy—the jumbo soft drink, the bag of chips, maybe something more substantial like a pizza slice, whatever it takes to replenish yourself for the interstate.

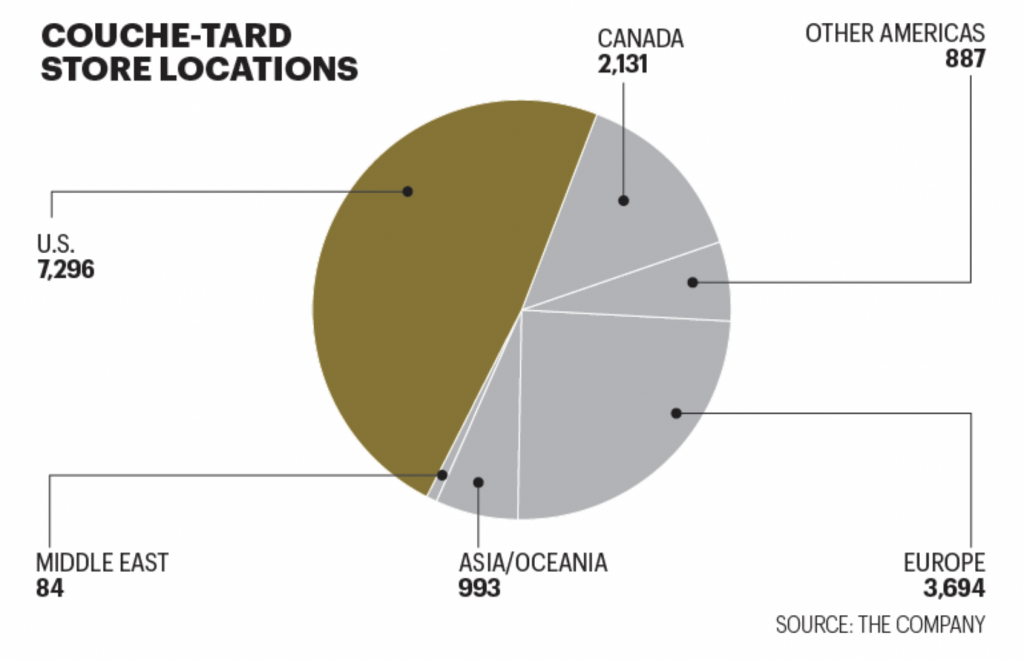

But what few drivers know is that this American road-trip ritual is increasingly likely to involve a huge Canadian company. CST Corner Stores in Texas and the Southeast, Holiday gas stations across the Northern Tier, and above all, Circle K just about everywhere in the U.S.: These familiar brands and others—making up 7,300 U.S. stores in all—belong to Alimentation Couche-Tard, a convenience-store giant headquartered in Laval, Quebec, outside Montreal.

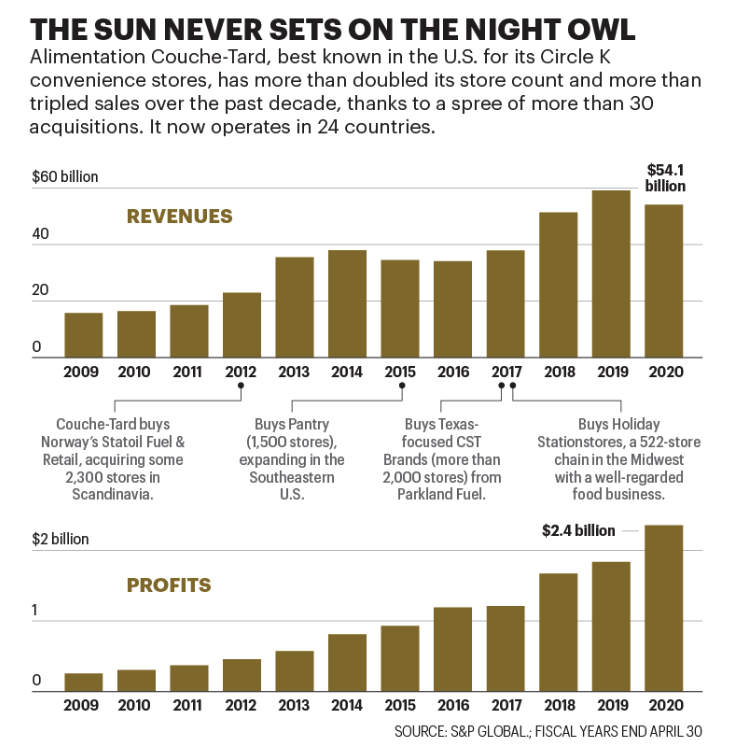

Having started in 1980 as a single store, Couche-Tard (pronounced “koosh-tar,” it means “late sleeper” or “night owl” in French) now owns or licenses more than 14,500 “c-stores” in a network that spans North America and Northern Europe, with outposts in Latin America, the Middle East, and Southeast Asia. Couche-Tard took in

$54 billion in sales in its 2020 fiscal year, making it Canada’s third-biggest company. But the U.S. accounts for 70% of its revenue, and its stateside footprint could get bigger. In late July, the company reportedly made an offer to buy the 3,900-store Speedway chain from Marathon Petroleum. Although that bid was unsuccessful, Couche-Tard has signaled that it’s still on the hunt.

Couche-Tard built this gas-station Goliath with savvy M&A—including 33 acquisitions big and small in the 2010s alone. The company aims to buy well-run retailers that it can help improve, rather than acting as turnaround artists. “They’re never looking for fixer-uppers or things that are broken,” says Moody’s senior analyst Louis Ko of Couche-Tard’s leaders.

But they are looking to keep growing. Brian Hannasch, an Iowa native who became Couche-Tard’s CEO in 2014, tells Fortune that the company’s ambitions were stymied by high valuations in recent years. “The market was frothy. Things traded at multiples that didn’t make sense to us,” says Hannasch. That has changed: The travel pullback resulting from the COVID-19 pandemic has hurt Couche-Tard’s sales, but it has also driven other chains’ values down to an affordable range

At the same time, Couche-Tard is relying on food to make its existing empire more profitable. The company posits that gas-station retail can be quality retail, with higher-margin merchandise: It doesn’t have to be day-old coffee and endless beef jerky. At hundreds of stores in the U.S. and Canada, the company is bringing in fresher food, installing espresso machines, and stocking wines that cost up to $50 a bottle. In Canada, where recreational marijuana use is legal, Couche-Tard is even exploring cannabis retail. “Couche-Tard is attracting a customer into their stores who’s not necessarily going in to fill up their gas tank,” says Derek Dley, an analyst at Canaccord Genuity.

Whichever strategies pay off, Couche-Tard has room to grow in a fragmented North American landscape. According to Euromonitor International, only two c-store brands command more than 5% of the U.S. market: Couche-Tard’s Circle K, with 5.7%, and 7- Eleven (owned by Japan’s Seven & I Holdings), with 10.7%. It was Seven & I that snared Speedway, for $21 billion, far more than Couche-Tard has ever spent on an acquisition. But the country is full of smaller chains that are ripe for takeovers and of hard-pressed energy companies eager to divest from gas-station retail—dynamics that should help Couche-Tard keep climbing the U.S. leaderboard.

Quebec has its own bustling convenience store culture. There, they’re called dépanneurs, from dépanner, to get someone out of a bind. Alain Bouchard, a native of Quebec’s remote Saguenay region, got his first c-store job as a preteen in the 1960s, helping his brother operate a location of a retailer called Perrette. He later worked at Provi-Soir, then the biggest Quebec chain, before striking out on his own in 1980, with his first Couche-Tard store.

M&A quickly became part of Couche-Tard’s MO. Bouchard gradually expanded in Quebec, culminating with the 1997 acquisition of Provi-Soir, whose winking-owl logo Couche-Tard adopted. The company then turned its attention south, cannily purchasing a few operations in the Midwest, where competition was lighter than in the Northeast. (One of those chains was Indiana-based Bigfoot, where Hannasch worked at the time.) In 2003 came the deal that made Couche-Tard a major U.S. player: It bought Circle K, with its 2,300 stores, for $821 million from ConocoPhillips, beating Blackstone and Morgan Stanley for the prize.

As a dealmaker, Couche-Tard developed an M&A discipline that helped it avoid the ill- considered mergers that have helped decimate the retail sector. Couche-Tard has been ultra-strict about not overpaying. It uses its own internal M&A SWAT team, rather than relying on costly, sometimes self-interested help from investment banks. (Bouchard, now chairman, still joins that team for big deals.) Before agreeing to the Circle K acquisition, Couche-Tard execs insisted on visiting 460 of the chain’s stores— to learn its strengths and weaknesses, to see what sold well where, and why, and to meet and win over the rank and file. When Circle K initially balked, Couche-Tard threatened to walk away.

Couche-Tard is organized into 26 highly decentralized operating units, so local chains don’t lose touch with their customers. “We don’t import a bunch of Canadians or a bunch of Americans,” says its CEO, Brian Hannasch, an Iowa native.

Once a chain becomes part of Couche-Tard, it’s likely to retain its identity (though not its brand name: Since 2015, Couche-Tard has rebranded most of its stores outside Quebec as Circle K). The company is organized into 26 operating units that are highly decentralized, so local chains don’t lose touch with their customers. Local managers tend to stay on, too. “We don’t import a bunch of Canadians or a bunch of Americans,” Hannasch says. Not that Couche-Tard lacks a unifying culture: When Hannasch joined the corporate team, his initiation included a fishing trip with Bouchard and his deputies where he had to sing traditional Québécois folk songs around a campfire, despite not speaking a lick of French.

Couche-Tard’s emphasis on autonomy makes the company unusually nimble for a retailer of its size. When COVID-19 struck Ireland in March, the government required home-improvement stores and nurseries to stay closed, leaving Emerald Isle green thumbs stranded as spring began. But Circle K gas stations were considered essential —and they spotted an opportunity. By April, the 406 Irish stores were selling plants, shrubs, and gardening tools to relieved horticulturists. Local management acted on its own, says Hannasch: “If we had waited for [headquarters in] Laval to say, ‘This is okay,’ we’d never have gotten it done.”

Couche-Tard has pulled off the balancing act to which all big retailers aspire: catering to local tastes while operating at massive scale. When Hannasch visited Latvia, he was put off to see soda stocked in Circle K aisles rather than refrigerated—until he learned that many Latvians like their soft drinks warm. “It’s not a chain of 9,000 locations,” says Louis Hébert, a professor at HEC Montreal business school who has studied Couche-Tard’s North American stores. “It’s 9,000 chains of one location.”

Ideas still flow downward from the parent company, of course. Couche-Tard advises store managers about product selection, often based on hyper-detailed analysis of store-by-store data. It is also testing dynamic pricing technology, which sets prices specific to a given store based on demand and local purchasing power. “It’s easier to charge $1.69 for a Pepsi at every store,” says Hannasch. “But if you take a couple of pennies here, a couple of pennies there, across 10,000 locations, it adds up quickly.”

These days, Couche-Tard is hunting for more pennies in the food-and-beverage aisles. Management has set an ambitious goal to double earnings before interest, taxes, depreciation, and amortization (Ebitda) to some $6 billion by 2023. Fuel generates 72% of company sales, but its margins are low. Nonfuel services and merchandise like food, on the other hand, represent 27% of sales but more than half of gross profit.

Food was the driving force behind one of Couche-Tard’s last big deals, the 2017 acquisition of Minnesota-based Holiday Stationstores. Holiday has a reputation for offering far better breakfast and sandwich fare than you’d expect from a gas station— think fresh food from offsite providers, rather than microwaved mush—and Couche- Tard is working to absorb its dining DNA.

Back home in Canada, Couche-Tard is exploring a business line that isn’t compatible with driving at all. It has teamed up with Canopy, a leading cannabis supplier, to open a proof-of-concept retail store in Ontario. And last year it bought a 9% stake in pot retailer Fire & Flower, with an option to become a majority owner. For Hannasch, this

is about getting ready for an inevitable new opportunity: “Eventually it will be legalized in most of the U.S.,” he says.

Underlying Couche-Tard’s bustle is an awareness that it can’t stand pat: After all, its top-selling product, fossil fuel, is in a long-term decline. In Norway, where Couche- Tard bought the retail business of state oil company Statoil in 2012, half of all new cars sold are electric. Today, Circle Ks in that nation are rapidly rolling out electric- vehicle charging hubs. They’re also doubling down on lattes and upscale baked goods, so that drivers have something to enjoy while they wait 20 minutes for a recharge. The takeaway: Couche-Tard wants to keep its gas-station empire thriving, even if gas stations stop selling gas.